Special report: The evolution of the European igaming market: from monopolies to a regulated industry

Focus Gaming News examines how, over the past ten years, the European Union consolidated its position as one of the igaming industry’s most important markets.

Special report.- A decade ago, the regulatory landscape for igaming in Europe was, at best, a patchwork of different rules. At worst, it was a legal limbo in which operators had to navigate state monopolies and arbitrary restrictions. Today, in 2026, that landscape looks entirely different.

This is the first in a series of special articles examining how the gambling industry has evolved over the past decade, the challenges it has faced, and what the future holds. In this issue, Focus Gaming News explores how Europe has become one of the most robust regulatory regions in the gambling industry.

The starting point: a fragmented Europe

Today, all EU member states have some form of licensing framework for igaming. The road to this point, however, was neither linear nor free of tension.

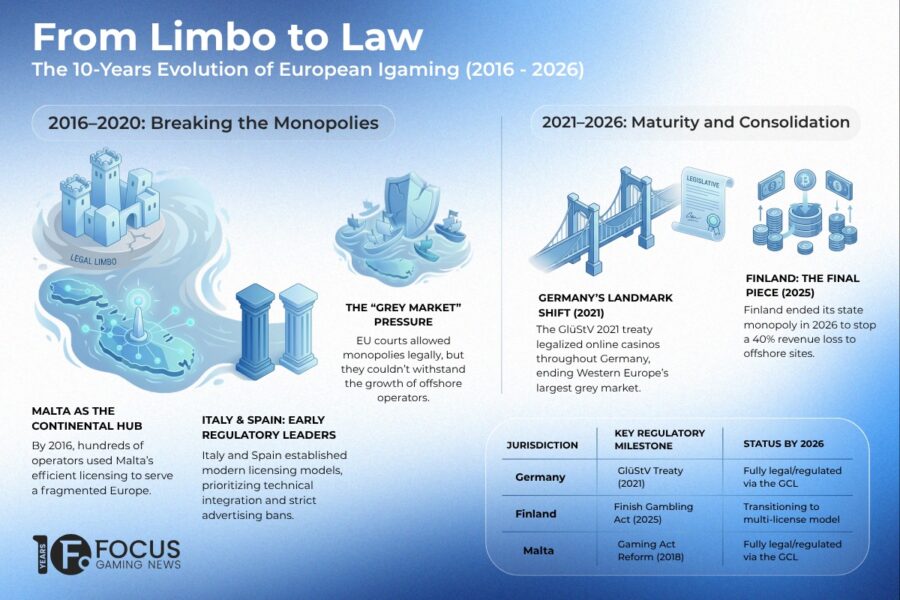

In 2016, the picture looked very different. Some countries, including the United Kingdom (with the Gambling Commission operating since 2014), France, Italy and Spain, had relatively established licensing regimes. But most of continental Europe operated under one of three logics: outright state monopoly, tacit prohibition, or regulatory permissiveness that delegated to Malta or Gibraltar the responsibility of licensing operators that were actively acquiring customers across the continent.

Malta was, in effect, the industry’s main hub. The Malta Gaming Authority (MGA) had built, since the early 2000s, a jurisdiction that combined regulatory seriousness, administrative efficiency and fiscal attractiveness. By 2016, hundreds of operators were based in Valletta or the surrounding area of Sliema. Malta was, in a sense, the industry’s answer to European fragmentation: if states did not want to regulate, the market would find someone who would.

But that model was under pressure. The European Commission had spent years pursuing infringement proceedings against countries that blocked access to operators licensed in other member states. The legal argument was clear: if online gambling was a service, the freedom to provide services under the Treaty on the Functioning of the EU should apply. States responded with the argument of “overriding reasons in the general interest” (consumer protection, fraud prevention, funding for national sport) and almost always won before the Court of Justice of the European Union.

The result was paradoxical: legally, monopolies could survive. In practice, however, they were unable to withstand the growing grey market.

Italy and regulatory maturity

Italy started 2016 with an advantage: its regulator, the ADM (“Agenzia delle Dogane e dei Monopoli”), had built one of the most comprehensive licensing regimes in Europe since 2011. Separate licences by vertical, strict technical requirements, integration with payment systems and a policy of excluding unlicensed operators that, despite room for improvement, worked better than in most countries.

What the 2016–2026 period brought Italy was, above all, consolidation, though political tensions were never far away and, in one way or another, continue to this day. The advertising ban on gambling (the so-called “Dignity Decree” of 2018) sparked a debate that remains unresolved, one that has since been replicated in other markets: can a regulated market function if it cannot communicate with its potential customers? The industry argued that the restriction only pushed players towards offshore operators.

Despite this, Italy became one of the most important markets in Europe. Its online gambling volumes grew steadily, and the ADM maintained a position of technical leadership among the continent’s regulators.

Spain: from pioneer architecture to a mature market

Spain was, in 2011, one of the first continental countries to build a modern licensing regime for online gambling. The DGOJ (Dirección General de Ordenación del Juego) established a framework that was, at the time, seen as a model.

The 2016–2026 decade was a story of gradual maturation for Spain. The 2020 pandemic accelerated the growth of online gambling abruptly — and with it came a sharp regulatory response: the new rules on gambling ads approved that year were among the strictest in Europe, limiting ads to late-night hours and banning the use of celebrities and athletes. However, by 2024–2025, the Spanish market was more concentrated, more mature and, according to operators working within it, one of the most demanding in terms of compliance.

Germany and the GlüStV 2021, and the case of Greece

If there is one moment that defines the decade in terms of regulatory impact in Europe, it is July 2021, when Germany’s Fourth Interstate Treaty on Gambling (Glücksspielneuregulierungsstaatsvertrag, or GlüStV 2021) came into force.

Context is essential to understanding the scale of the change. Until that point, Germany was Western Europe’s largest grey market. The EU’s most populous and highest-GDP country operated under a legal framework in which online casino gambling was, in practice, a grey area: banned in most of the country under state legislation, yet with operators licensed in Malta or Gibraltar actively acquiring millions of German players with no real consequences.

The GlüStV 2021 changed that. For the first time, online casinos and online poker were legalised throughout Germany under the supervision of the newly established Gemeinsame Glücksspielbehörde der Länder (GGL), which is based in Halle.

The early years were difficult. The GGL took longer than expected to issue licences, the illegal market remained robust, and several operators decided against applying for a German licence, given the cost-benefit analysis. From 2024 onwards, however, the market began to stabilise, and the GGL gained institutional experience.

Asked to comment for this article, the GGL declined to answer the questions put to it, though its written communication noted that “the 16 federal states in Germany took a significant and correct step in 2021 toward an effective regulation and a supervision of the cross-state gambling market in Germany.” The authority also said it “maintains a regular exchange with other European regulatory authorities, which is an important part of our work. This allows us to share best practices and gain insights from the experiences of our European counterparts, further supporting the continuous improvement of fighting illegal online-gambling in Germany.”

Greece is another clear example of this broader trend. Over much of the past decade, the Hellenic Gaming Commission developed a licensing framework that became increasingly demanding. It set strict entry criteria, imposed substantial ongoing reporting obligations and showed a clear readiness to enforce the rules. By the mid 2020s, the Greek market had attracted several operators and positioned itself as one of the more solid regulatory environments in southeastern Europe.

The case of Finland: the last piece of the puzzle

Until 2025, Finland was the only EU member state still operating a full state monopoly on gambling. That changed when President Alexander Stubb signed the new Finnish Gambling Act, bringing Veikkaus’s monopoly over online gambling to an end.

The decision was pragmatic rather than ideological: according to the Finnish Competition Authority, approximately 50 per cent of Finnish online gambling spend was going to unlicensed offshore operators. As a result, Veikkaus had lost 40 per cent of its GGR over five years, and its revenue fell 3.6 per cent year-on-year in 2025.

From July 2027, the Finnish market for sports betting, online casino and slots will be open to competition under licences supervised by the new Finnish Supervisory Agency. Veikkaus will retain its monopoly over lotteries and land-based casinos, but will compete for the first time in the online space.

However, according to Mika Kuismanen, the CEO of the Finnish Trade Association for Online Gambling, the reform was carried out at least ten years too late. In an exclusive interview with Focus Gaming News, he said: “A dramatic decline in the channelisation rate has been visible for a long time, but the political courage to break the monopoly has been lacking.”

Malta reinvents itself

While the major markets were building their own regulatory frameworks, Malta had to answer an existential question: What role does a small jurisdiction play when the large markets start regulating directly?

The answer came in 2018 with the approval of a new Gaming Act. The overhaul was profound: it simplified the licensing structure from four categories to two, strengthened corporate governance and compliance requirements, bolstered the MGA’s supervisory tools and sent a clear signal that Malta intended to become synonymous with quality.

The bet paid off. Malta consolidated its position as the reference jurisdiction for operators seeking access to European markets where igaming was not yet formally regulated at a national level, and as an operational base of excellence for companies with a global presence. The relationship between the MGA and emerging national regulators was also significant: Malta shared technical know-how and accumulated experience that many eastern and northern European countries used as a reference when building their own frameworks.

Charles Mizzi, CEO of the Malta Gaming Authority, said the 2018 reform was the defining moment of the decade: “The reform marked a shift towards a principles‑based, technology‑neutral regulatory framework, allowing the Authority to regulate an increasingly complex and fast‑moving sector more effectively. It provided the foundation on which several other key initiatives were built, including the introduction of a dedicated Player Protection Directive, stronger sports betting integrity requirements, and the extension of integrity reporting obligations to B2B licensees.

“Equally significant was the Authority’s decision to embrace innovation early. By launching a policy framework for Distributed Ledger Technologies and Virtual Financial Assets, Malta became the first gaming regulator to formally regulate the use of blockchain and cryptocurrencies within gaming operations. This sent a clear signal that innovation and regulatory oversight are not mutually exclusive.

“Beyond the domestic framework, the launch of the Authority’s International Affairs Strategy was another important milestone. It strengthened Malta’s role in global regulatory cooperation and reflected a recognition that effective regulation increasingly depends on cross‑border engagement.

“Finally, the introduction of the voluntary ESG Code of Good Practice for the remote gaming sector – the first holistic sustainability framework of its kind introduced by a gaming regulator – demonstrated how regulation can go beyond compliance to actively shape responsible and sustainable industry behaviour.

“Together, these initiatives reflect an evolution in regulatory philosophy: maintaining strong standards while adopting a more evidence-led and risk-based approach to supervision. This enables the Authority to focus oversight where it is most needed for player protection, market integrity, and compliance. As the industry evolves, we are building on this foundation, including ongoing work on an upcoming AI Gaming Charter to guide the responsible use of artificial intelligence in the sector.”

Asked whether there was anything he would have approached differently, Mizzi said: “Regulation is never static, particularly in a sector as dynamic as gaming. Over the past decade, the industry has evolved rapidly, driven by technological innovation, new business models, and shifting consumer expectations. The experience of the past decade has reinforced the importance of building adaptability into the regulatory framework.

“Rather than identifying a specific decision that should have been taken differently, the key lesson from this period is therefore the importance of building regulatory frameworks that are sufficiently flexible to evolve alongside the industry. The MGA has increasingly focused on risk-based supervision, stronger engagement with stakeholders, and early consideration of emerging technologies such as distributed ledger technology and artificial intelligence.

“What this experience reinforces is the need for regulators to remain agile, to review their tools regularly, and to ensure that oversight keeps pace with innovation while continuing to safeguard consumers and the integrity of the sector.”

The EGBA’s role: driving harmonisation

Throughout this period of fragmented national regulation, the European Gaming and Betting Association (EGBA) played a significant role. Founded in 2007 to represent the leading licensed online operators before EU institutions, it gradually evolved over the decade into an organisation focused on technical standards, social responsibility and direct dialogue with national regulators.

Its most tangible contributions included the development of interoperability protocols for self-exclusion systems, a work that helped pave the way for initiatives such as GAMSTOP in the United Kingdom and equivalent programmes on the continent, as well as technical publications on responsible gambling and a consistent presence in European Parliament debates on a possible EU-wide framework directive for gambling regulation.

That debate, however, remains unresolved. The industry has repeatedly asked whether the EU will ever produce a directive harmonising minimum requirements across member states. The EGBA has consistently advocated for one, but member states have with equal consistency resisted any binding harmonisation initiative. The result is that Europe remains, to this day, a regulatory patchwork where coordination depends more on the goodwill of individual regulators than on any common framework.

The view from operators

For operators that had to navigate this period, the multiplication of regulatory regimes was simultaneously an opportunity and an operational challenge. Each new regulated market represented access to players previously unreachable through legal channels. But it also meant a new set of technical requirements, compliance obligations, reporting standards, local payment integrations and product adaptations.

Large pan-European operators developed complex compliance structures, with teams dedicated to each jurisdiction and technology to manage regulatory differences at scale. Mid-sized and smaller operators faced a choice: specialise in specific markets or absorb the cost of diversification.

Technology providers (platforms, risk management systems, responsible gambling tools) enjoyed some of their strongest growth during this period, precisely because regulatory fragmentation was driving demand for solutions that could help manage the complexity.

Focus Gaming News spoke to Henrik Gedda, head of regional sales Nordic & Eastern Europe at Play’n GO, and Marina Zacharopoulou, senior compliance manager at Altenar, about how each company’s presence in Europe changed over the past decade and how they navigated the shifting regulatory landscape.

Gedda said: “Over the past decade, Europe has transformed into one of the most mature and strictly regulated igaming regions in the world — and our growth has been built on embracing that evolution, not resisting it.

“Play’n GO has always taken the long‑term view that sustainable success comes from operating in regulated markets, and the last ten years have proved that philosophy right.

“As the landscape shifted, we adapted early and decisively: prioritising compliance, strengthening responsible gaming measures, and ensuring our portfolio delivered entertainment that meets both player expectations and regulatory requirements.

“Our expansion across Europe mirrors this disciplined approach. We have steadily increased our footprint to operate in more than 35 regulated jurisdictions worldwide, with more to add to that list this year, but Europe remains the core foundation of that network.

“What’s been vital is the mindset — treating regulation as a catalyst for innovation rather than a constraint. Whether addressing evolving compliance frameworks, adapting to advertising restrictions, or aligning with new responsible gaming standards, we’ve consistently invested in the technology, processes, and talent needed to meet and exceed expectations.”

Zacharopoulou said: “From a compliance standpoint, the last decade has been anything but linear. When I joined Altenar, we were already holding our MGA licence and had established a footing in the UK — but the real complexity came as more European markets moved toward national licensing. Romania was one of our earlier milestones, followed by Greece’s framework under the Hellenic Gaming Commission in 2021, Sweden’s regime in the summer of 2023, and Denmark in January 2025. Each market required us to build out an entirely separate compliance stack, not just tick a box and move on.

“What we got right was building for modularity early. The architecture was already designed to absorb those changes at the compliance layer without disrupting the core platform.

“As a B2B supplier, our compliance responsibilities are distinct from those of operators — we’re not directly managing player relationships, but we do carry real obligations around technical standards, reporting, and making sure our platform equips operators with everything they need to meet their own RG requirements. That’s a meaningful distinction that shapes how we approach each new jurisdiction.

“Operating across Malta, Romania, the UK, Sweden, Denmark and Greece simultaneously means managing six different regulatory calendars and six sets of reporting obligations. That demands proper internal structure — not a generalist approach.”

On which regulatory decisions had the greatest impact on their growth trajectory, Gedda said: “Europe’s regulatory transformation over the last decade, and particularly the shift away from fragmented or grey‑market conditions toward robust, individual national licensing, has shaped Play’n GO’s trajectory in profound ways. Markets that implemented clear, consistent frameworks allowed us to deepen our presence, invest confidently and build long‑term partnerships with operators.

“Crucially, as more governments moved toward higher scrutiny and stricter responsible gaming expectations, it validated the exact direction we had already taken as a business. Decisions that emphasised consumer protection, game integrity, and sustainable operation aligned perfectly with our own philosophy.

“For example, as various European jurisdictions took a tougher view on game features like Bonus Buy, our long‑standing stance against including such mechanics — because we believe they do not contribute to a sustainable entertainment ecosystem — meant we were already well positioned for compliance and continued growth.”

Zacharopoulou said: “Sweden’s licensing regime, introduced in summer 2023, is one I point to most often. The Spelinspektionen framework was strict by design — and intentionally so. Operators and suppliers who had been operating comfortably without proper structure found themselves locked out quickly. For us, having already invested in the right compliance infrastructure, it became a competitive advantage almost overnight.

“Greece is the market I’ve watched transform most significantly. The Hellenic Gaming Commission has built something genuinely robust — the licensing criteria are serious, the ongoing reporting requirements are substantive, and the regulator has shown it’s willing to enforce. Obtaining our licence there gave us early positioning in a market that has since attracted serious, well-capitalised operators. Each of these wasn’t just a compliance exercise — it was a commercial signal to operators that we could support them wherever they wanted to grow.”

What remains unresolved

Today, the European online gambling map looks radically different from 2016. Several challenges, however, remain.

The illegal market persists. In virtually every regulated market, unlicensed operators retain significant market share, particularly among segments of players who prioritise product offering over regulatory safety.

Consistency between jurisdictions remains fragmented. An operator licensed in ten European countries operates under ten different sets of rules, with differences in betting limits, responsible gambling requirements, reporting obligations and advertising conditions. The cost of compliance is high and acts as a barrier to entry for smaller players.

The advertising question is unresolved. Italy, Spain and several other countries have opted for strict restrictions. Others maintain more permissive frameworks. There is no European consensus on the right balance between consumer protection and the viability of the legal market.

On the main drivers of growth and the key challenges facing the sector in the coming years, Zacharopoulou said: “Finland is the clearest near-term structural opportunity. The move away from Veikkaus’s monopoly toward a licensed multi-operator model is the most significant regulatory shift happening in Europe right now. When a monopoly market opens, the compliance bar tends to be set high from day one — the regulator is under pressure to demonstrate the new framework works. Suppliers who aren’t prepared will struggle to get their operators across the line. We’ve been through this process enough times to know how to get ahead of it, and Finland is on our radar.

“On challenges: the cost of compliance across multiple jurisdictions is consistently underestimated. Licence fees, GGR taxes, technical audits, ongoing reporting obligations — it compounds fast. For operators, this makes the choice of B2B partner increasingly consequential. You want a supplier whose compliance infrastructure is already built out, not one that makes your regulatory burden heavier.”

Gedda said: “There is a tremendous opportunity ahead for Europe, but the industry must continue to evolve. For Play’n GO, the growth drivers are clear: a deeper shift toward entertainment‑first gaming, as players increasingly demand experiences defined by narrative, audio design, and innovative mechanics — not just wagering structures. Our focus on immersion, storytelling, and responsible enjoyment will continue to resonate strongly across Europe.

“Continued innovation in game mechanics is also key. Europe remains a fertile ground for breakthrough formats. Our recent advances, from next‑generation grid slots to new mechanics such as Blitzways and GO Ultra, show how pushing boundaries will fuel long‑term engagement.

“As we’ve seen in the UK with the success of transitioning iconic titles like Book of Dead into retail environments, the blend of digital IP with physical casino experiences will open new growth channels across Europe.

“Europe will continue tightening its regulatory frameworks, and we believe that’s a good thing — provided the industry embraces sustainability as its guiding principle. Advertising restrictions, enhanced compliance requirements, and heightened public scrutiny will all demand operational discipline and a true commitment to responsible gaming. Working closely with the regulators will be key to make sure we foster a safe and entertaining environment for all.

“The suppliers and operators who succeed will be those who treat entertainment quality and player protection as inseparable. That’s the future we believe in, and the direction we’re committed to leading.”

A decade of institution-building

What happened in Europe between 2016 and 2026 was, in essence, a massive process of institution-building. Countries that had never had to think seriously about how to regulate igaming were forced to do so — sometimes hastily, always under pressure from multiple actors with competing interests: operators, consumers, governments, European institutions and public health organisations.

On the level of cooperation between European regulators over the period and where he sees room for improvement, Mizzi said: “Cooperation with European and international gambling regulators has strengthened significantly over the past decade and remains a cornerstone of the Authority’s regulatory approach. In the absence of full regulatory standardisation across jurisdictions, alignment and cooperation with our counterparts are essential to maintaining robust, effective and credible oversight of a cross‑border industry.

“The MGA actively enters into Memoranda of Understanding and data‑sharing agreements with international authorities, which are critical tools for enhancing supervisory effectiveness, facilitating the exchange of information and building mutual trust. Our participation in mechanisms such as the EU/EEA Cooperation Arrangement for Member States enables structured and timely information‑sharing on issues that affect the gaming sector across borders.

“We also maintain a strong presence within key international fora, including the Gaming Regulators European Forum (GREF) and the International Association of Gaming Regulators (IAGR). These platforms provide valuable opportunities to exchange best practices, engage in constructive dialogue and contribute to greater convergence in regulatory thinking, while ensuring that national perspectives are understood and respected.

“At the same time, there is clear scope for further progress. Greater regulatory standardisation at European level, particularly in areas such as anti‑money laundering and player protection, would benefit both regulators and licensees. More aligned requirements would help reduce the compliance burden created by a patchwork of differing national rules, while supporting more consistent supervisory outcomes and higher overall standards of protection.

“Finally, the Authority places strong value on knowledge‑sharing with regulators from emerging and unregulated jurisdictions, through bilateral visits and cooperation initiatives. These engagements contribute to raising global standards, strengthening integrity and supporting the long‑term sustainability of the gaming sector internationally.”

Europe now has regulators with technical expertise, legal frameworks that assign rights and obligations to operators, and an industry that, for the most part, prefers to operate within the rules rather than outside them.

Ten years ago, that was far from obvious. That it is today is, in itself, an extraordinary achievement.

This article is the first instalment of a series produced by Focus Gaming News to mark its tenth anniversary. Over the course of 2026, the articles will examine the most defining moments that shaped the global igaming industry between 2016 and 2026, from regulatory changes and market openings to technological shifts and the rise of new regions. Each piece will be accompanied by exclusive interviews with the executives, regulators and analysts who were part of these changes.