South Africa, Tanzania and Kenya share igaming demand but produce different market outcomes: Blask

A Blask report for Focus Gaming News reveals that identical demand conditions across South Africa, Tanzania and Kenya in 2025 have led to fundamentally different market outcomes, driven by structure, competition and regulatory constraints.

Special Report.- South Africa, Tanzania and Kenya all experienced broadly similar demand curves throughout 2025, shaped by the same global sports calendar. However, the markets built on top of that shared rhythm looked nothing alike. Betting followed the same pattern in all three countries: a mid-year dip, recovery from July, and a peak around the Africa Cup of Nations (AFCON 2025). However, how that demand was ultimately captured reflected the distinct structure, competitive dynamics and regulatory environment in each country.

The latest Blask report for Focus Gaming News shows that activity across all three markets softened when European football slowed, returned from mid-year and built into a pronounced year-end peak driven by AFCON. The Blask Index captures real-time igaming demand through normalised search data, while BAP (Brand’s Accumulated Power) measures how that demand is distributed across operators.

Where the story turns is in what happens after demand is captured. South Africa holds its shape, Tanzania concentrates around a dominant leader, and Kenya remains unsettled. The same cycle plays out in each market, but the outcomes diverge sharply once structure, competition, and regulation come into play.

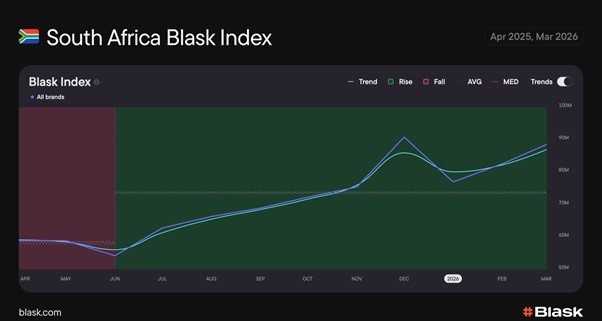

South Africa: a stable duopoly

South Africa shows a mature growth pattern: steady expansion with short-term volatility rather than structural breaks. The April to June dip is a seasonal lull, not a structural shift: with fewer major sporting events in play, engagement naturally falls away, and the broader trajectory holds.

As the calendar strengthens, momentum returns. European football resumes, the FIFA Club World Cup adds weight, and local events carry betting volumes through the second half of the year before AFCON concentrates activity into a December peak.

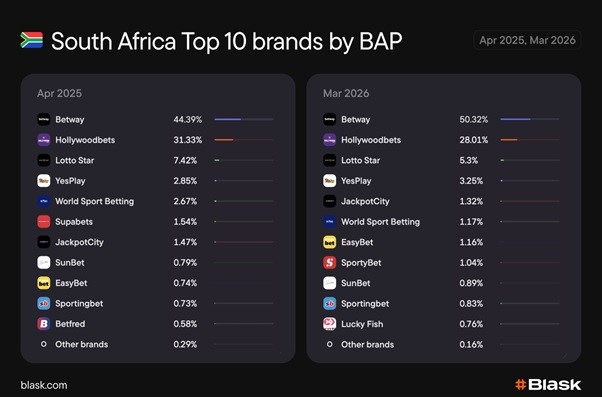

What does not change is control. Betway and Hollywoodbets continue to dominate, accounting for close to 80 per cent of total demand, while LottoStar remains well behind at around five per cent BAP. The market grows, but the hierarchy holds.

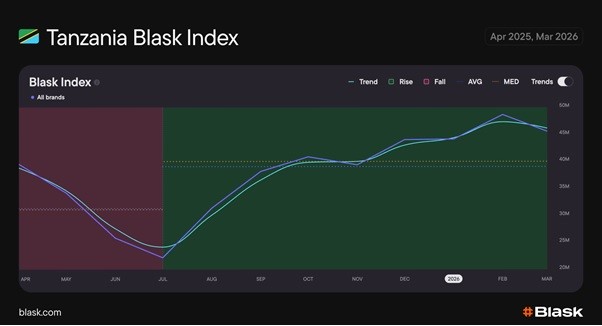

Tanzania: growth under a dominant leader

Tanzania shows a recovery-driven growth pattern: a clear decline in the first half of the year followed by strong expansion through Q4. The sports calendar was thin in the early months, with no major tournaments to sustain betting activity, and engagement drifted lower.

That began to shift as football returned in volume. CAF competitions, European leagues, World Cup qualifiers and AFCON brought players back, gradually restoring momentum.

The gains, however, are concentrated. betPawa retains a dominant position, controlling roughly two-thirds of total demand. The bigger shift sits behind the leader: SportyBet has displaced Betway to take second place, climbing to around 12 per cent BAP, while the rest of the field remains fragmented below the 10 per cent mark. Year-on-year dynamics point to steady underlying expansion, with betPawa recording growth of 20.8 per cent and SportyBet climbing by 54.6 per cent, reinforcing a structure that continues to revolve around a single leading operator.

Kenya: a contested top under pressure

Kenya is the only market in the group that has not shown sustained growth. Demand moves in cycles, with repeated declines offsetting short-term recoveries, shaped by regulation as much as by the sports calendar.

The slide set in after December 2024. A nationwide advertising suspension and tighter marketing rules began to limit acquisition, while the end of the European football season and the absence of a mid-year AFCON removed key engagement drivers. By mid-2025, activity had weakened significantly.

A mid-year lift followed, driven by the FIFA Club World Cup, the return of the Premier League and tax changes that reduced per-bet friction, but the momentum did not hold. New tax structures introduced later in the year raised transaction costs, advertising restrictions remained in place, and World Cup qualification setbacks cooled national-team engagement. Activity turned downward again.

A brief December uplift, supported by AFCON and seasonal betting patterns, has not carried into 2026, with the market settling at a lower level. Demand is event-driven but structurally capped, with each recovery offset by regulatory and economic constraints.

The instability is reflected in operator rankings. Betika remains the leader but has weakened year-on-year. Odibets has dropped from second to fourth place, while GameMania has moved up to the runner-up spot and SportPesa has nearly doubled its demand to climb from sixth to third. betPawa, by contrast, continues to compress alongside the broader top of the market. No operator is consolidating control, and the “Other” segment continues to account for a significant share of demand. Leadership exists, but it is neither stable nor consolidating.

The sports calendar sets the tempo; market structure decides the outcome

Across all three markets, demand has followed the same underlying rhythm, a calendar-driven cycle built around European football and AFCON, with a mid-year dip and a second-half recovery. What differs is how that demand is ultimately captured.

Where regulation is stable, growth compounds into the hands of incumbents. Where it is not, each recovery gets clipped before it can consolidate.